Under the right circumstances, refinancing student loans can be a good money saver. It might help you get a lower interest rate, get a fixed rate from a variable interest, consolidate your loans into monthly payments, and let go of a co-signer. This is a win-win situation in debt management.

Before you choose to refinance your loan, you need to get the distinction between refinancing and consolidation. When you refinance, you are getting a new loan in place of your old loan, while consolidation means you will be simplifying things by combining your many different loans into one loan.

Types of Loans to Refinance

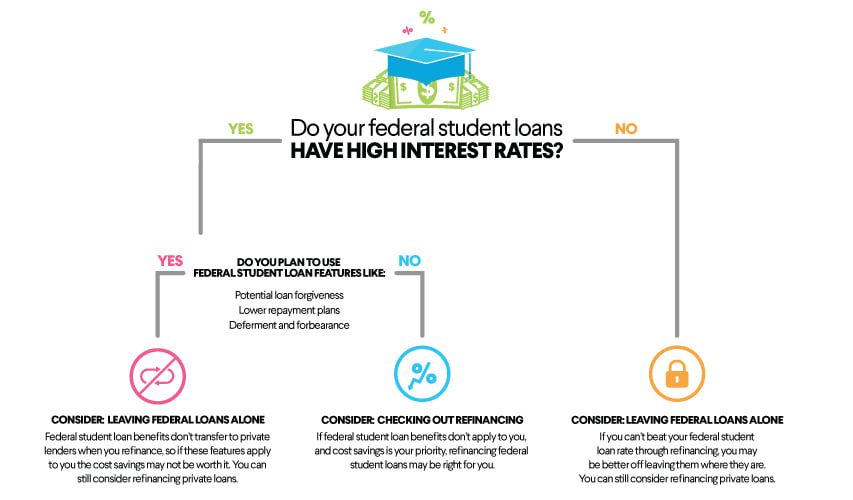

First, you need to understand that the United States government cannot refinance student loans. It can only consolidate them. You cannot change your federal student loan for another with a lower interest rate or transform a private student loan into a federal one.

If you choose to consolidate a federal student loan via the Department of Education, you might end up paying higher interest rates.

Private student loan refinancing will let you refinance a federal student loan or a private loan—or both combined—to be one private loan. But refinancing is close to impossible for federal student loans.

If you do so, you minimize your chances of getting government assistance programs, most importantly, enrollment in an income-driven repayment plan.

This plan reduces your payment to an amount in line with your discretionary income. It cancels any loan balance left if you have not completed payments for your federal loans by the repayment time elapses.

Lastly, while several private lenders can temporarily lower or stop loan repayments, they avoid default by deferring or forbearing. Such terms do not seem to be appealing compared to federal student loans.

Suppose you are a teacher or a public service employee seeking loan forgiveness under one government-offered program. In that case, you will not qualify for the benefit anymore if you want to refinance student loans.

When You Should Refinance Student Loans

You can only consider refinancing if:

- You have a strong credit score to get you a lower interest rate than the one you have

Student loan refinancing eligibility requires your FICO credit score should be at 650, but you get better rates that promise more cash flow if your score is higher. If refinancing a loan still leaves more money for you to live your daily life, retirement plans, and get out of debt, then it is worth considering.

Read Also: How to improve your credit score

- You want to change the loan from a variable interest rate to a fixed-rate loan.

When your loan has a variable interest rate, there is a likelihood that the interests may go up further with the changes in the market rate. If it happens, then getting a new fixed-rate loan could be much cheaper. This is also applicable if you took a high-interest private loan.

A borrower who is still repaying a student loan with high-interest rates and high balances may find it easy to save up some money with a lowered rate.

- You want to lower your monthly payments

If you have many private student loans, you could choose to refinance student loans so they can be counted as a single loan that will require you to make only one payment monthly.

In reducing a federal student loan without taking a private loan, the process is called consolidation and not refinancing student loans. Your new federal direct consolidation loan would have an interest rate weighted average of your existing loans.

If you want to take full responsibility for refinancing a student loan in your name, you could take out a co-signer from your debt liability. However, some lenders will allow a co-signer to release only after you have made a few consecutive payments for two years or four years. Even after making such payment obligations, you need to meet some credit requirements.

- You do not mind giving up federal benefits.

If you are in an extraordinary financial situation and the refinancing benefits are more than the cost of forgoing your federal loans. It might be the right thing to do.

- You want to let go of a co-signer

Reasons to Avoid Refinancing Student Loans

Do not go for a refinance if you are unclear about the benefits. There are no ground rules concerning how much money you need to have saved to make a refinance viably, but it should be worth your efforts and unforeseen costs.

Even though lower interest rates may make one believe it is the best time to refinance federal student loans, the timing may not favor those eligible for affordable repayment programs or forbearance.

If you have a hard time paying off your student loan or want a reduced monthly payment, keep the federal program with emergency and payment options better than refinancing. Almost half of all federal student loans are replayed through an income-driven repayment plan.

If you want to get loan forgiveness, or you still want to get the relief benefits, do not consider refinancing.

If you are a parent who is still repaying private or federal loans that you took to pay for your child, you might be thinking of refinancing your loans through a home equity loan or cash-out refinance mortgage loan is worth it.

However, most of these options need you to make usually higher upfront costs, and your home will be used as collateral. Defaulting would make you lose your home, which is a considerable risk.

Refinancing student loans is still possible if you recently declared bankruptcy, but it will not be easy. For student loan refinance qualification, there should be a certain amount of time since your bankruptcy. It could be anywhere between four to ten years.

It might be hard for borrowers who have defaulted on student debt to get a refinance. Any loan default in the past is a huge red flag for lenders. Suppose your default is taken out from your credit reports, a process that could take up to seven years.

In that case, you may be eligible for the refinance if you meet the credit score threshold, increased income, and other necessary criteria.

In cases where your loan repayment periods take longer, it might be hard for you to get a refinance. Getting a low monthly payment loan could imply getting a longer loan repayment period and paying higher interest.

For example, if you take a loan on a 10-year term, getting a new 10-year to refinance loan would mean that you pay for a total of 15 years. Calculating the difference, you will realize that the interest rates will be higher than what you would have paid in a ten-year repayment plan.

Preparing your student loan refinancing

Once you decide to refinance student loans, you cannot take the decision lightly. You cannot revert your choice once you have committed to the refinance. You need to understand the benefits and downsides that would follow if you make a move.

If you have known every detail of the process, you can proceed to refinance student loans, most specifically considering the low-interest rates when it is availed. Here are a few steps you can take:

- Decide whether refinancing student loans is the best option

Refinancing student loans is only reasonable if you want to save money, but not for everyone. It would be best to have strong credit and a stable income to be eligible for the lowest interest rates and meet your lender’s lending criteria.

The moment you take that route, you lose the chance to get government repayment programs such as student loan relief. Only consider refinancing if your job is at risk and these options are not applicable.

Refinancing private student loans is not riskier since these benefits are not involved.

- Compare different lenders

In the beginning, most refinance lenders are similar, but it would be better if you consider features that handle your situations. You might find that the processing fees are slightly different, or the interest rates and repayment periods differ from one to the other.

- Consider many rate estimates

Once you land lenders that serve you better, look at all their rate estimates. The one with the lowest interest rates is the best option to go with. You can compare different lenders and settle for the one with the best rates and terms.

As you look for a better option, some lenders will want you to pre-qualify—give primary data which provides the best estimate of your qualifying rate. You will have to complete applications for some lenders, but the rate issued will be an offer.

Pre-qualifying will not affect your credit scores in any way, and only an application may deeply check into your credit hence lowering your scores.

Read Also: Should You Consolidate Your Student Loans?